Study of the VIX

There is plenty of analysis out there about the stock market. Much of this analysis is on an intraday basis, analyzing how individual stocks moves based on oil prices or geopolitical turmoil. Sometimes these explanations have an obvious correlation to the markets; other times, these explanations are nothing more than educated guesses. Instead, we're interested in long-term trends. This week, we study the relationship between the VIX index and the S&P 500.

VIX Index

The VIX index is primarily used as a representation of the market's expectations of the 30-day volatility of the stock market, expressed in percentage points.Specifically, the VIX is 100 times the square root of the expected 30-day variance of the S&P 500 rate of return.

Where Var is annualized expected 30-day variance. The expected 30-day variance is estimated by the forward price of S&P 500 options with 30 days to expiration, e^(rt), where S is the spot price. The forward prices of S&P 500 options represent the market's risk-neutral expectation of the variance of the underlying.

No arbitrage pricing says that the forward price of variance must equal the forward price of its replicating portfolio. Since holding forward positions in a portfolio do not contribute value to the portfolio at the present, the forward price of variance must equal the forward price of the options. If 30-day options are not available, the VIX is calculated using a weighted average of forward prices of options with expirations close to 30 days.

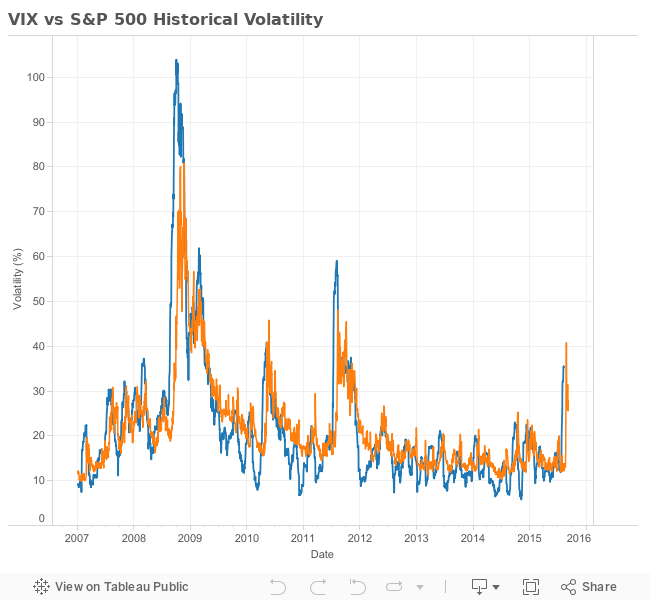

We can see that the VIX follows the general shape of the S&P 500's forward 30-day volatility, but with a lag of a few days. This indicates that the VIX is good at determining the level of volatility in the next 30 days, but not at predicting large changes in volatility. Moreover, for high levels of S&P 500 forward volatility, such as in the beginning of October 2008 following Lehman's bankruptcy and preceding several DJIA increases and declines, the VIX seems to underestimate the level of volatility in the next 30 days. Generally, however, the VIX seems to remain above the actual S&P 500 volatilities.

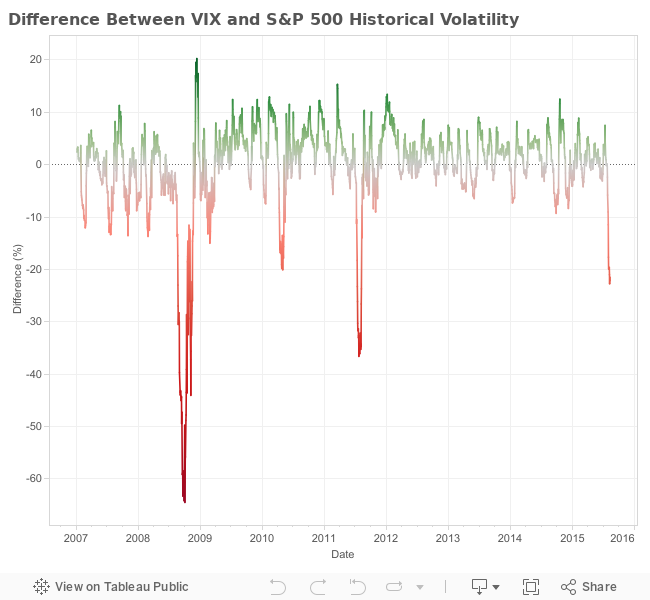

The difference between the VIX and the historical S&P 500 volatilities shows points in time where the VIX is significantly lower. These include the end of September 2008 and the beginning of October 2008, which as we mentioned before, included the worst of the financial crisis. These low VIX points also include the end of April 2010, which preceded the May 6 "Flash Crash", a trillion-dollar stock market crash that lasted just minutes. Another dip in the VIX compared to the S&P 500 was at the end of July 2011, which preceded an August 2011 stock market crash due to a US credit downgrade. The last VIX dip in the graph is due to the recent China crisis. These are all points of high S&P volatility in the first graph that the VIX severely underestimates.